FAQ Strategies

FAQ

- How do I use warrants to “hedge” my position?

- How do I use the Cash Extraction Strategy?

- How do I use the Barbell Strategy?

- How do I use the “Last Defense Strategy” for Naga Matrix?

- Can I perform Technical Analysis on Structured Warrants charts?

- How do I select warrants based on OTM, ATM & ITM?

- Shouldn’t I be looking at Implied or Historical Volatility?

- Is warrant trading of shariah compliant stocks also shariah compliant?

- Why is the Structured Warrants always priced as RM0.150 on your Term Sheets? If on Day 1, the warrant is trading at RM0.070, is the warrant trading at a discount?

- What is Delta, Gamma, Theta and Vega?

- The Greeks - Shouldn’t I be looking at Delta, Gamma, Theta or Vega?

1. How do I use warrants to “hedge” my position?

This strategy is for traders that wish to protect an existing position by entering an opposing position. Examples include,

Risk hedging - The purpose of this strategy is to reduce the market risk linked to a security portfolio. There is a way of hedging the risk by taking a position opposite to the existing one on the market. This may mean buying a put or call warrant, depending on the asset.

Offsetting a risk position through the purchase of a warrant - If an investor expects that stock prices will fall, he/she can hedge his stock portfolio by acquiring put warrants that entitle him to sell his shares at a predetermined price - e.g. at the current market price - within the period stipulated in the warrant contract. In doing so, he will prevent the value of his portfolio from decreasing.

The investor must pay a price, in the form of a warrant premium, to protect his assets. However, this price is far lower than the loss he would incur as a result of the expected downturn in the market.

With the liquidity and leverage effect provided, investors may enter a put warrant at a fraction of the price of underlying to protect its portfolio from the downside. Given this, the maximum loss is kept at your investment principle.

For the purposes of risk management, warrants can be a very low-risk and protective instrument.

2. How do I use the Cash Extraction Strategy?

Cash Extraction Strategy suggesting investors to instead putting all the cash towards the underlying (mother share), investors can enter the warrants by considering the relevant delta exposure. With this approach, investors can hold the same exposure in the counter while holding some extra cash.

Securing capital & obtaining liquidity - At times of uncertainty, investors seek to profit from eventual market rallies without compromising the capital they initially invested, i.e. securing the capital.

By deploying this strategy, you can free up capital without forgoing the potential future returns by selling off a portion of stock exposure & purchasing a portion of structured warrants. This also protects your portfolio by limiting the risk of future losses to the invested premium.

As a warrant’s expiration date draws nearer, if an investor wants to roll over his/her strategy, he/she can sell the warrants in his/her portfolio and buy other warrants on the same underlying asset with a later expiration date.

3. How do I use the Barbell Strategy?

The Barbell Strategy suggests investors to hold a larger portion of their portfolio in low-risk, low-return products while allocating a smaller portion into higher-risk, high-return products.

This strategy allows investors make extra ROI (Return on Investment) as compared to investing fully in underlying (so called mother share), and yet protect their capital in less-risky assets like the underlying asset, given the leveraging effect in warrants. This is by increasing the average returns of the whole portfolio, boosted by amplified returns in structured warrants.

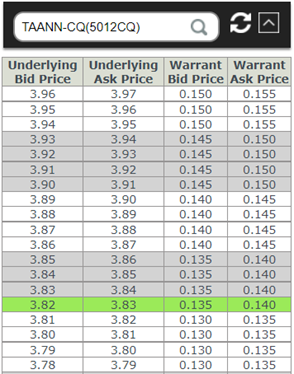

4. How do I use the “Last Defense Strategy” for Naga Matrix?

Last Defense Strategy suggest that instead of entering warrant and wait for price to flip (very much depends on the sensitivity of the warrants), investor may enter just before the flipping point to ensure greater breakeven/profit opportunity with the use of Naga Matrix.

Example on the below matrix, investors could enter 0.135 when the underlying is quoting at 3.82/3.83. When the share price continues to go higher at 3.83/3.84, the trade is easily breakeven.

For example, traders can consider entering a position by buying TAAN-CQ at RM0.135, when TAAN-CQ is Bid RM0.130/0.135 Ask & its underlying stock TAAN is RM3.81/RM3.82

When TAAN is RM3.82/3.83, TAAN-CQ will be Bid RM0.135/0.140

This allows traders to avoid uncertainty, and break-even effortlessly.

5. Can I perform Technical Analysis on Structured Warrants charts?

No, please don’t. Structured warrants are derivative of the underlying share. Structured warrants follow the underlying’s share price movement like a child follows its mother.

You may perform Technical Analysis on the underlying price chart, and enter a position via Structured Warrant.

6. How do I select warrants based on OTM, ATM & ITM?

OTM (Out-the-money) warrants typically having have lesser sensitivity towards the movement in share price while ITM (In-the-money) warrants typically having extreme sensitivity over the share price.

If you are a short-term trader aiming to benefit from the short-term movement of the underlying, ATM (At-the-money) and ITM (In-the-money) warrants will best suit your appetite.

Whereas for long-term trader aiming to maximize profit by entering the warrant, OTM (Out-the-money) may be considered for higher profitability.

7. Shouldn’t I be looking at Implied or Historical Volatility?

Investors should look at Implied Volatility as it represents current and forward market, whilst Historical Volatility refers to previous volatility which could serve as reference.

8. Is warrant trading of shariah compliant stocks also shariah compliant?

No, trading structured warrant is not Shariah-compliant even though the underlying is given its derivative characteristic.

9. Why is the Structured Warrants always priced as RM0.150 on your Term Sheets? If on Day 1, the warrant is trading at RM0.070, is the warrant trading at a discount?

Price fixing at minimum of 15 sen is a regulatory requirement. The price the Issuer quotes on Day 1 Listing Day is the Fair Price.

10. What is Delta, Gamma, Theta and Vega?

Delta: Measures the rate of change of the price of the option with respect to a move in the underlying asset.

Gamma: Measure of the delta’s change relative to the changes in the price of the underlying asset. If the price of the underlying asset increases by $1, the option’s delta will change by the Gamma amount. The main application of gamma is the assessment of the option’s delta.

Theta: Measure of the sensitivity of the option price relative to the option’s time to maturity. If the option’s time to maturity decreases by one day, the option’s price will change by the Theta amount. The Theta option Greek is also referred to as time decay.

Vega: Measures the sensitivity of an option price relative to the volatility of the underlying asset. If the volatility of the underlying asset increases by 1%, the option price will change by the Vega amount.

11. The Greeks - Shouldn’t I be looking at Delta, Gamma, Theta or Vega?

Investors should look at Delta to gauge the exposure of the warrant in terms of underlying share (taking into account the warrant conversion ratio). While Gamma, Theta, and Vega is more relevant to market-maker as these are the parameters for their hedging activity.

Investors may consider Delta to gauge the exposure of the warrant in terms of underlying share.

The M.E.S.T.I. strategy we recommend already includes this Delta component in the “E” for Effective Gearing

Effective Gearing = Delta x Gearing

Gamma, Theta, and Vega however, is more relevant to Market-makers as these are the parameters for their hedging activity.